Facts About How Do Reverse Mortgages Work Example Revealed

The longer you prepare on living there, the better the opportunity that home loan points will be worth it. With a home mortgage calculator, you can figure out precisely how long that is and whether or not home mortgage points deserve it in your situation. In addition, you do require to weigh in tax benefits, the accessibility of outside investments, and your cash on hand.

Generally, the expense of a home loan point is $1,000 for every $100,000 of your loan (or 1% of your overall mortgage amount). Each point you buy reduces your APR by 0. 25% (what are reverse mortgages and how do they work). For instance, if your rate is 4% and you buy one point, your APR rate would go down to 3.

Because your rate is lower, you will conserve a little bit on every one of your home mortgage payments. Eventually, over time, those cost savings will increase and equal and go beyond the amount you had to spend for the discount rate. This is referred to as the break-even point. Home mortgage calculators can help you figure out precisely where that break-even point is.

If you keep your home longer than the break-even point, you'll start to recognize some cost savings. Bear in mind, however, that all other conditions stay the exact same. Numerous would argue that you need to also determine the cash you could have made over that duration by putting the cash you spent on points in another type of investment.

( the focus of this story) lower the interest rate on your loan and lower your month-to-month payments. Mortgage points provide you the choice to decrease your rates of interest and reduce your month-to-month mortgage payments. There are two kinds of these points: discount points and origination points. Discount rate points are a form of pre-paid interest that you can buy to decrease your rate of interest.

The Definitive Guide to Why Are Most Personal Loans Much Smaller Than Mortgages And Home Equity Loans?

These likewise assist decrease the rate of interest on your mortgage. In many cases, you'll pay a charge equal to 1% of the home loan quantity for each discount rate poinot. This fee is typically paid directly to your lending institution or as part of a fee package. Most lending institutions supply the option for property buyers to acquire home loan points, though they are not needed to.

Usually, this is topped out around 4 or 5 points. Some lending institutions will let you acquire in increments, so you may not require to purchase entire points if you're looking for a more customized fit. Home loan points may be tax-deductible, depending upon whether you meet the criteria set out by the Internal Revenue Service.

While the majority of people will be able to deduct mortgage points over the life of the loan, you should meet several particular criteria to deduct them all during the first year. These are plainly set out on the Internal Revenue Service site. 4% rates of interest with no mortgage points 3. 875% rate of interest with 1 point4%, No points$ 477 - what does arm mean in mortgages.

513.875%, 1 point$ 467. 38$ 168,257. 40 N/A$ 10. 04$ 3,612. 11If you pay 1 point, which will cost you $1,000 on a $100,000 home loan (remember, each point costs 1% of your house loan amount) to get the 3. 875% rate, you lower your regular monthly payments by about $10. That suggests it would take 100 regular monthly payments, or more than 8 years, to recover the upfront cost of that point.

do you actually prepare to stay in your home for 30 years? And offering or re-financing prior to the break-even point implies you'll in fact wind up paying extra interest on the loan. Richard Bettencourt, a home mortgage broker in Danvers, Massachusetts, and previous president of the Association of Home loan Experts, states paying home loan points typically isn't a great financial relocation." The only way I see a point making good sense is for that rarity of the person who states, 'I'm going to make all 360 payments (on a 30-year house loan) and never ever move,'" he said.

Rumored Buzz on Which Bank Is The Best For Mortgages

Another way to look at mortgage points is to think about just how much cash you can pay for to pay at the loan-closing table, states Mark Palim, vice president of applied economic and housing research study for Fannie Mae, a government-owned business that purchases home mortgage debt." If you utilize up some of your savings towards prepaying your interest, which makes your payment lower on a monthly basis, you have less cost savings if the hot water heater breaks," he stated.

If you know you're in your home for the long https://gumroad.com/jeovislseo/p/the-main-principles-of-what-happens-to-mortgages-in-economic-collapse run, you might profit of lower monthly home loan payments for the next couple of years. On the other hand, mortgage points most likely aren't worth it if you 'd be using a big portion of your savings to buy them. Lowering your month-to-month payments by a little quantity doesn't rather make good sense if you 'd have to compromise your emergency fund to do it particularly if you're not committed to remaining in your home for the next 30 years.

If you're intending on remaining in your house longer than the break-even point, you will see cost savings. If those savings surpass what you might get in outside financial investment, then home loan points will certainly be worth it. Additionally, you ought to consider the need for capital to purchase home loan points. When you buy a house, you have to pay for many things like the deposit, closing expenses, moving costs and more.

In financing, Basis Points (BPS) are a system of measurement equivalent to 1/100th of 1 percent. BPS are utilized for measuring rates of interest, the yield of a fixed-income securityFixed Income Bond Terms, and other percentages or rates used in finance. This metric is commonly utilized for loans and bonds to signify portion changes or yield spreads in monetary instruments, especially when the difference in product rate of interest is less than one percent.

01 percent or 1/100th of 1 percent. The prospering points move up gradually to 100%, which equates to 10000 basis points, as shown in the diagram listed below. PercentageBasis Points0. 01% 10. 1% 100. 5% 501% 10010% 1000100% 10000Examples: The difference in between bond interest rates of 9. 85 percent and 9. 35 percent is 0. 5 percent, comparable to 50 basis points.

The Ultimate Guide To What Is An Underwriter In Mortgages

Due to the development of iPhone sales, Apple Inc. reported high revenues, more than what was estimated; the stockStock increased 330 BPS, or 3. 3 percent, in one day. To transform the variety of basis indicate a portion and, in turn, a percentage to basis points, without utilizing a conversion template or chart, evaluate the following: Basis points to percentage Divide the points by 100Percentage to basis points Increase the percentage by 100The main reasons investors use BPS points are: To describe incremental rates of interest changes for securities and rate of interest reporting.

The Only Guide for How Do Buy To Let Mortgages Work Uk

The longer you intend on living there, the much better the possibility that home loan points will deserve it. With a home mortgage calculator, you can identify exactly for how long that is and whether or not home loan points deserve it in your circumstance. In addition, you do require to weigh in tax advantages, the availability of outside financial investments, and your money on hand.

Typically, the expense of a home mortgage point is $1,000 for every $100,000 of your loan (or 1% of your overall home mortgage amount). Each point you purchase lowers your APR by 0. 25% (how many mortgages are there in the us). For example, if your rate is 4% and you buy one point, your APR rate would decrease to 3.

Because your rate is lower, you will conserve a little bit on every one of your home mortgage payments. Eventually, gradually, those cost savings will increase and equivalent and exceed the amount you needed to https://gumroad.com/jeovislseo/p/the-main-principles-of-what-happens-to-mortgages-in-economic-collapse pay for the discount. This is understood as the break-even point. Home mortgage calculators can assist you identify precisely where that break-even point is.

If you keep your home longer than the break-even point, you'll begin to realize some cost savings. Bear in mind, though, that all other conditions stay the exact same. Numerous would argue that you have to also compute the cash you could have earned over that period by putting the cash you invested on points in another form of financial investment.

( the focus of this story) lower the rates of interest on your loan and decrease your month-to-month payments. Home loan points offer you the alternative to decrease your rate of interest and decrease your month-to-month home mortgage payments. There are two types of these points: discount rate points and origination points. Discount rate points are a kind of prepaid interest that you can buy to reduce your interest rate.

The Best Strategy To Use For When Did 30 Year Mortgages Start

These also assist reduce the rates of interest on your home mortgage. In a lot of cases, you'll pay a charge equivalent to 1% of the mortgage amount for each discount poinot. This cost is typically paid directly to your loan provider or as part of a cost package. A lot of lending institutions offer the alternative for property buyers to purchase mortgage points, though they are not needed to.

Typically, this is topped out around four or five points. Some lending institutions will let you buy in increments, so you may not need to buy whole points if you're looking for a more customized fit. Home loan points might be tax-deductible, depending on whether you fulfill the criteria set out by the Internal Revenue Service.

While the majority of people will have the ability to deduct mortgage points over the life of the loan, you should fulfill numerous specific criteria to deduct them all throughout the very first year. These are clearly laid out on the IRS site. 4% interest rate without any mortgage points 3. 875% rates of interest with 1 point4%, No points$ 477 - what are the lowest interest rates for mortgages.

513.875%, 1 point$ 467. 38$ 168,257. 40 N/A$ 10. 04$ 3,612. 11If you pay 1 point, which will cost you $1,000 on a $100,000 home mortgage (keep in mind, each point costs 1% of your mortgage quantity) to get the 3. 875% rate, you lower your regular monthly payments by about $10. That means it would take 100 monthly payments, or more than 8 years, to recover the in advance expense of that point.

do you really plan to remain in your house for 30 years? And selling or re-financing before the break-even point means you'll actually end up paying extra interest on the loan. Richard Bettencourt, a home mortgage broker in Danvers, Massachusetts, and previous president of the Association of Mortgage Experts, states paying home loan points generally isn't a great monetary move." The only method I see a point making good sense is for that rarity of the individual who says, 'I'm going to make all 360 payments (on a 30-year mortgage) and never ever move,'" he stated.

Indicators on How To Compare Lenders For Mortgages You Should Know

Another way to look at home mortgage points is to think about just how much cash you can manage to pay at the loan-closing table, states Mark Palim, vice president of applied economic and housing research for Fannie Mae, a government-owned company that purchases mortgage debt." If you consume a few of your cost savings towards prepaying your interest, that makes your payment lower on a month-to-month basis, you have less savings if the hot water heater breaks," he stated.

If you know you're in your home for the long haul, you may profit of lower monthly home loan payments for the next couple of decades. On the other hand, mortgage points most likely aren't worth it if you 'd be utilizing a huge portion of your cost savings to purchase them. Decreasing your regular monthly payments by a small quantity doesn't quite make sense if you 'd have to sacrifice your emergency situation fund to do it specifically if you're not devoted to remaining in your home for the next thirty years.

If you're intending on remaining in your home longer than the break-even point, you will see cost savings. If those cost savings exceed what you might get in outdoors financial investment, then mortgage points will undoubtedly deserve it. In addition, you must consider the requirement for capital to purchase mortgage points. When you purchase a house, you have to spend for many things like the down payment, closing expenses, moving costs and more.

In financing, Basis Points (BPS) are an unit of measurement equal to 1/100th of 1 percent. BPS are used for measuring rates of interest, the yield of a fixed-income securityFixed Income Bond Terms, and other portions or rates used in finance. This metric is commonly utilized for loans and bonds to signify portion changes or yield spreads in monetary instruments, particularly when the difference in material interest rates is less than one percent.

01 percent or 1/100th of 1 percent. The prospering points move up gradually to 100%, which equals 10000 basis points, as highlighted in the diagram below. PercentageBasis Points0. 01% 10. 1% 100. 5% 501% 10010% 1000100% 10000Examples: The distinction between bond rates of interest of 9. 85 percent and 9. 35 percent is 0. 5 percent, equivalent to 50 basis points.

The smart Trick of How To Calculate Extra Principal Payments On Mortgages That Nobody is Talking About

Due to the growth of iPhone sales, Apple Inc. reported high profits, more than what was estimated; the stockStock increased 330 BPS, or 3. 3 percent, in one day. To convert the variety of basis indicate a percentage and, in turn, a percentage to basis points, without using a conversion design template or chart, examine the following: Basis indicate percentage Divide the points by 100Percentage to basis points Increase the portion by 100The main factors financiers utilize BPS points are: To explain incremental rates of interest modifications for securities and rates of interest reporting.

Not known Facts About What Is The Current Apr For Mortgages

Where the property costs more than the quantity owed to the lender, the debtor or his estate will receive the extra funds. According to the October 2018 filings of the Office of the Superintendent of Financial Institutions (OSFI), an independent federal firm reporting to the Minister of Financing in that month, the outstanding reverse home loan debt for Canadians soared to $CDN3.

Daniel Wong at Better House wrote that, the dive represented a 11. 57% increase from September, which is the second greatest boost considering that 2010, 844% more than the mean monthly pace of development. The yearly increase of 57. 46% is 274% bigger than the mean annualized rate of development. Reverse home loans in Canada are offered through two financial organizations, HomEquity Bank and Equitable Bank, although neither of the programs are insured by the government.

To get approved for a reverse mortgage in Canada, the customer (or both customers if wed) need to be over a certain age, at least 55 years of age the borrower need to own the property "entirely or nearly"; in addition, any outstanding loans protected by your home needs to be retired with the profits of the reverse mortgage there is no qualification requirement for minimum income level.

The exact amount of money available (loan size) is figured out by a number of aspects: the borrower's age, with greater quantity offered for greater age existing interest rates residential or commercial property value, consisting of place and a factor for future gratitude program minimum and optimum; for example, the loan may be constrained to a minimum $20,000 and an optimum of $750,000 The interest rate on the reverse home mortgage varies by program (how did subprime mortgages contributed to the financial crisis).

Exact costs depend on the particular reverse home mortgage program the customer acquires. Depending on the program, there might be the list below types of expenses: Real estate appraisal = $150$ 400 Legal advice = $450$ 700 Other legal, closing, and administrative expenses = $1,750 Of these costs, just the realty appraisal is paid upfront (out of pocket); the remaining expenses are instead deducted from the reverse mortgage proceeds.

" The cash from the reverse home loan can be used for any function: to repair a house, to spend for at home care, to deal with an emergency situation, or just to cover everyday costs." The customer keeps title to the residential or commercial property, including unused equity, and will never ever be required to abandon your home.

This consists of physical maintenance and payment of all taxes, fire insurance coverage and condo or upkeep fees. Money received in a reverse home loan is an advance and is not gross income - what to know about mortgages in canada. It for that reason does not affect federal government advantages from Aging Security (OAS) or Guaranteed Income Supplement (GIS). In addition, if reverse mortgage advances are used to purchase nonregistered investmentssuch as Surefire Investment Certificates (GICs) and shared fundsthen interest charges for the reverse home loan may be deductible from investment income earned. [] The reverse home loan comes duethe loan plus interest should be repaidwhen the borrower passes away, sells the residential or commercial property, or vacates your house.

How What Credit Score Do Banks Use For Mortgages can Save You Time, Stress, and Money.

Prepayment of the loanwhen the debtor pays the loan back before it reaches termmay sustain charges, depending on the program. In addition, if rate of interest have actually dropped since the reverse home mortgage was signed, the mortgage terms might include an "' interest-rate differential' penalty." In Canada a reverse home mortgage can not collect financial obligation beyond the fair market value of the home, nor can the lender recover losses from the homeowner's other assets.

Here is a helpful. pdf titled: what do I do when my loan is due? https://www. nrmlaonline.org/what-do-i-do-when-my-loan-is-due The FHA-insured House Equity Conversion Home Loan, or HECM, was signed into law on February 5, 1988, by President Ronald Reagan as part of the Real Estate and Community Advancement Act of 1987. The very first HECM was provided to Marjorie Mason of Fairway, Kansas, in 1989 by James B.

According to a 2015 article in the, in 2014, about 12% of the United States HECM reverse home loan debtors defaulted on "their home taxes or property owners insurance" a "reasonably high default rate". In the United States, reverse mortgage borrowers can deal with foreclosure if they do not preserve their homes or maintain to date on property owner's insurance coverage and real estate tax.

HUD particularly cautions consumers to "be careful of scam artists that charge countless dollars for information that is totally free from HUD. To certify for the HECM reverse mortgage in the United States, customers normally should be at least 62 years of age and the house must be their main house (2nd homes and financial investment homes do not qualify).

Under the old guidelines, the reverse mortgage might just be written for the partner who was 62 or older. If the older partner passed away, the reverse home loan balance ended up being due and payable if the more youthful surviving spouse was ended of the HECM loan. If this younger partner was not able to pay off or re-finance the reverse home loan balance, she or he was forced either to offer the home or lose it to foreclosure.

Under the new standards, partners who are more youthful than age 62 at the time of origination retain the protections used by the HECM program if the older partner who got the mortgage dies. This suggests that the surviving spouse can stay living in the home without needing to pay back the reverse mortgage balance as long as she or he stays up to date with property taxes and house owner's insurance and preserves the home to an affordable level.

Nevertheless, borrowers do have the option of paying for their existing home mortgage balance to get approved for a HECM reverse mortgage. The HECM reverse home loan follows the standard FHA eligibility requirements for property type, suggesting most 14 family homes, FHA authorized condos, and PUDs certify. Manufactured homes likewise qualify as long as they meet FHA standards.

What Are Interest Rates Today On Mortgages - Truths

An approved counselor should help explain how reverse home mortgages work, the monetary and tax ramifications of taking out a reverse mortgage, payment alternatives, and expenses related to a reverse mortgage. The therapy is indicated to secure customers, although the quality of counseling has actually been slammed by groups such as the Consumer Financial Defense Bureau.

On March 2, 2015, FHA implemented brand-new standards that require reverse mortgage applicants to go through a monetary evaluation. Though HECM borrowers are not needed to make month-to-month mortgage payments, FHA desires to make sure they have the monetary capability and desire to stay up to date with residential or https://writeablog.net/voadillx3v/you-can-discover-more-details-on-how-this-works-a commercial property taxes and house owner's insurance (and any other appropriate home charges).

What Are The Current Refinance Rates For Mortgages Things To Know Before You Get This

The longer you plan on living there, the much better the opportunity that home mortgage points will deserve it. With a mortgage calculator, you can determine precisely the length of time that is and whether or not mortgage points deserve it in your scenario. Furthermore, you do require to weigh in tax benefits, the accessibility of outdoors financial investments, and your money on hand.

Typically, the expense of a home loan point is $1,000 for every single $100,000 of your loan (or 1% of your total home loan quantity). Each point you purchase decreases your APR by 0. 25% (what does ltv mean in mortgages). For instance, if your rate is 4% and you buy one point, your APR rate would decrease to 3.

Due to the fact that your rate is lower, you will save a little bit on each of your home mortgage payments. Ultimately, gradually, those savings will increase and equal and go beyond the quantity you had to spend for the discount. This is called the break-even point. Mortgage calculators can help you determine precisely where that break-even point is.

If you keep your home longer than the break-even point, you'll start to realize some savings. Remember, however, that all other conditions remain the same. Many would argue that you need to likewise determine the cash you could have earned over that duration by putting the cash you invested on points in another type of investment.

( the focus of this story) lower the rates of interest on your loan and minimize your regular monthly payments. Home mortgage points give you the choice to reduce your rate of interest and decrease your regular monthly home loan payments. There are 2 kinds of these points: discount points and origination points. Discount rate points are a kind of prepaid interest that you can purchase to minimize your interest rate.

Getting The Which Of The Following Is Not True About Reverse Annuity Mortgages? To Work

These also help decrease the interest rate on your home mortgage. In many cases, you'll pay a fee equal to 1% of the home mortgage amount for each discount rate poinot. This cost is usually paid straight to your lending institution or as part of a cost package. Most lending institutions supply the alternative for property buyers to acquire home loan points, though they are not needed to.

Typically, this is topped out around 4 or 5 points. Some loan providers will let you purchase in increments, so you may not need to purchase whole points if you're trying to find a more customized fit. Home mortgage points might be tax-deductible, depending on whether you meet the criteria laid out by the Internal Revenue Service.

While many people will be able to subtract home loan points over the life of the loan, you need to fulfill a number of particular requirements to subtract them all throughout the first year. These are clearly laid out on the Internal Revenue Service website. 4% interest rate without any home loan points 3. 875% rate of interest with 1 point4%, No points$ 477 - what is the interest rates on mortgages.

513.875%, 1 point$ 467. 38$ 168,257. 40 N/A$ 10. 04$ 3,612. 11If you pay 1 point, which will cost you $1,000 on a $100,000 home loan (remember, each point expenses 1% of your mortgage amount) to get the 3. 875% rate, you lower your monthly payments by about $10. That indicates it would take 100 monthly payments, or more than 8 years, to recoup the upfront expense of that point.

do you truly plan to remain in your home for thirty years? And offering or refinancing before the break-even point suggests you'll actually end up paying additional interest on the loan. Richard Bettencourt, a home mortgage broker in Danvers, Massachusetts, and former president of the Association of Home mortgage Professionals, says paying home loan https://gumroad.com/jeovislseo/p/the-main-principles-of-what-happens-to-mortgages-in-economic-collapse points normally isn't an excellent monetary relocation." The only way I see a point making good sense is for that rarity of the person who says, 'I'm going to make all 360 payments (on a 30-year home loan) and never move,'" he said.

All About What Are The Best Banks For Mortgages

Another way to take a look at mortgage points is to think about how much cash you can pay for to pay at the loan-closing table, says Mark Palim, vice president of applied financial and real estate research for Fannie Mae, a government-owned company that buys home loan financial obligation." If you consume a few of your cost savings towards prepaying your interest, which makes your payment lower on a regular monthly basis, you have less cost savings if the water heating unit breaks," he said.

If you understand you're in your home for the long run, you may profit of lower regular monthly mortgage payments for the next few years. On the other hand, mortgage points most likely aren't worth it if you 'd be utilizing a huge chunk of your savings to buy them. Decreasing your month-to-month payments by a percentage does not quite make good sense if you 'd need to compromise your emergency situation fund to do it especially if you're not dedicated to remaining in your home for the next 30 years.

If you're planning on staying in your home longer than the break-even point, you will see savings. If those cost savings exceed what you might get in outside financial investment, then home mortgage points will unquestionably be worth it. Additionally, you should factor in the need for capital to buy home loan points. When you buy a house, you have to spend for lots of things like the down payment, closing expenses, moving costs and more.

In financing, Basis Points (BPS) are an unit of measurement equivalent to 1/100th of 1 percent. BPS are used for determining rate of interest, the yield of a fixed-income securityFixed Earnings Bond Terms, and other percentages or rates used in financing. This metric is frequently used for loans and bonds to symbolize percentage modifications or yield spreads in monetary instruments, particularly when the distinction in material rate of interest is less than one percent.

01 percent or 1/100th of 1 percent. The succeeding points go up gradually to 100%, which equates to 10000 basis points, as illustrated in the diagram listed below. PercentageBasis Points0. 01% 10. 1% 100. 5% 501% 10010% 1000100% 10000Examples: The difference between bond rates of interest of 9. 85 percent and 9. 35 percent is 0. 5 percent, equivalent to 50 basis points.

How What Is The Interest Rate Today For Mortgages can Save You Time, Stress, and Money.

Due to the development of iPhone sales, Apple Inc. reported high incomes, more than what was estimated; the stockStock increased 330 BPS, or 3. 3 percent, in one day. To transform the variety of basis points to a percentage and, in turn, a portion to basis points, without utilizing a conversion design template or chart, review the following: Basis indicate portion Divide the points by 100Percentage to basis points Increase the portion by 100The main factors financiers use BPS points are: To explain incremental rates of interest changes for securities and rates of interest reporting.

Which Type Of Organization Does Not Provide Home Mortgages? Can Be Fun For Everyone

Where the residential or commercial property sells for more than the amount owed to the lending institution, the customer or his estate will receive the extra funds. According to the October 2018 filings of the Office of the Superintendent of Financial Institutions (OSFI), an independent federal company reporting to the Minister of Finance in that month, the exceptional reverse home loan debt for Canadians skyrocketed to $CDN3.

Daniel Wong at Better Residence composed that, the dive represented a 11. 57% increase from September, which is the second biggest increase considering that 2010, 844% more than the mean regular monthly speed of growth. The yearly boost of 57. 46% is 274% larger than the mean annualized speed of growth. Reverse mortgages in Canada are offered through two financial institutions, HomEquity Bank and Equitable Bank, although neither of the programs are guaranteed by the federal government.

To get approved for a reverse mortgage in Canada, the borrower (or both customers if married) must be over a particular age, at least 55 years of age the debtor must own the residential or commercial property "completely or nearly"; in addition, any impressive https://writeablog.net/voadillx3v/you-can-discover-more-details-on-how-this-works-a loans secured by your home should be retired with the profits of the reverse home mortgage there is no credentials requirement for minimum income level.

The precise amount of cash offered (loan size) is determined by a number of factors: the customer's age, with higher amount readily available for greater age current rates of interest residential or commercial property value, including location and a factor for future gratitude program minimum and maximum; for example, the loan might be constrained to a minimum $20,000 and an optimum of $750,000 The interest rate on the reverse home mortgage differs by program (how do buy to rent mortgages work).

Specific expenses depend upon the particular reverse home mortgage program the debtor acquires. Depending on the program, there might be the list below types of costs: Realty appraisal = $150$ 400 Legal suggestions = $450$ 700 Other legal, closing, and administrative costs = $1,750 Of these expenses, just the genuine estate appraisal is paid upfront (out of pocket); the remaining costs are rather subtracted from the reverse home mortgage profits.

" The cash from the reverse home mortgage can be utilized for any purpose: to fix a home, to spend for at home care, to deal with an emergency situation, or merely to cover everyday costs." The customer maintains title to the property, including unused equity, and will never ever be forced to leave your house.

This includes physical upkeep and payment of all taxes, fire insurance coverage and condo or upkeep costs. Cash received in a reverse mortgage is an advance and is not taxable earnings - who has the best interest rates on mortgages. It for that reason does not impact government gain from Old Age Security (OAS) or Guaranteed Earnings Supplement (GIS). In addition, if reverse home loan advances are utilized to acquire nonregistered investmentssuch as Guaranteed Financial Investment Certificates (GICs) and shared fundsthen interest charges for the reverse home loan may be deductible from financial investment earnings earned. [] The reverse home loan comes duethe loan plus interest must be repaidwhen the borrower dies, offers the home, or vacates your house.

The Ultimate Guide To What Are Today's Interest Rates On Mortgages

Prepayment of the loanwhen the borrower pays the loan back before it reaches termmay sustain penalties, depending on the program. In addition, if rates of interest have actually dropped because the reverse home mortgage was signed, the home loan terms might include an "' interest-rate differential' charge." In Canada a reverse mortgage can not build up debt beyond the reasonable market price of the home, nor can the lending institution recover losses from the property owner's other assets.

Here is a convenient. pdf entitled: what do I do when my loan is due? https://www. nrmlaonline.org/what-do-i-do-when-my-loan-is-due The FHA-insured Home Equity Conversion Home Mortgage, or HECM, was signed into law on February 5, 1988, by President Ronald Reagan as part of the Real Estate and Neighborhood Development Act of 1987. The first HECM was provided to Marjorie Mason of Fairway, Kansas, in 1989 by James B.

According to a 2015 short article in the, in 2014, about 12% of the United States HECM reverse home loan debtors defaulted on "their property taxes or homeowners insurance" a "relatively high default rate". In the United States, reverse home loan debtors can face foreclosure if they do not keep their homes or maintain to date on property owner's insurance and real estate tax.

HUD specifically cautions customers to "be careful of scam artists that charge thousands of dollars for details that is complimentary from HUD. To get approved for the HECM reverse home loan in the United States, borrowers normally must be at least 62 years of age and the home should be their primary residence (2nd houses and financial investment homes do not certify).

Under the old guidelines, the reverse home mortgage might only be written for the spouse who was 62 or older. If the older partner passed away, the reverse home mortgage balance became due and payable if the more youthful enduring spouse was ended of the HECM loan. If this more youthful partner was unable to pay off or refinance the reverse home loan balance, she or he was forced either to sell the home or lose it to foreclosure.

Under the brand-new guidelines, partners who are more youthful than age 62 at the time of origination keep the securities provided by the HECM program if the older partner who got the home mortgage passes away. This means that the making it through partner can stay living in the house without needing to pay back the reverse home mortgage balance as long as she or he stays up to date with home taxes and house owner's insurance and maintains the home to a sensible level.

However, customers do have the choice of paying down their existing home loan balance to certify for a HECM reverse home loan. The HECM reverse home mortgage follows the basic FHA eligibility requirements for property type, meaning most 14 family residences, FHA approved condominiums, and PUDs certify. Made homes likewise qualify as long as they fulfill FHA requirements.

The Definitive Guide to What Is The Debt To Income Ratio For Conventional Mortgages

An authorized counselor should assist discuss how reverse mortgages work, the monetary and tax implications of securing a reverse mortgage, payment alternatives, and costs connected with a reverse home loan. The therapy is meant to safeguard borrowers, although the quality of counseling has actually been criticized by groups such as the Consumer Financial Defense Bureau.

On March 2, 2015, FHA executed brand-new standards that require reverse home loan candidates to go through a monetary assessment. Though HECM customers are not needed to make regular monthly mortgage payments, FHA wants to make certain they have the monetary ability and determination to stay up to date with residential or commercial property taxes and house owner's insurance (and any other applicable residential or commercial property charges).

Excitement About When Did 30 Year Mortgages Start

Where the home offers for more than the amount owed to the lender, the debtor or his estate will receive the extra funds. According to the October 2018 filings of the Office of the Superintendent of Financial https://writeablog.net/voadillx3v/you-can-discover-more-details-on-how-this-works-a Institutions (OSFI), an independent federal firm reporting to the Minister of Financing because month, the outstanding reverse home mortgage debt for Canadians soared to $CDN3.

Daniel Wong at Better Home composed that, the dive represented a 11. 57% increase from September, which is the second most significant boost because 2010, 844% more than the average month-to-month rate of growth. The annual increase of 57. 46% is 274% larger than the mean annualized pace of growth. Reverse mortgages in Canada are readily available through 2 banks, HomEquity Bank and Equitable Bank, although neither of the programs are guaranteed by the government.

To certify for a reverse home mortgage in Canada, the debtor (or both debtors if married) must be over a particular age, a minimum of 55 years of age the debtor need to own the residential or commercial property "entirely or nearly"; in addition, any exceptional loans protected by your house should be retired with the profits of the reverse mortgage there is no certification requirement for minimum earnings level.

The precise amount of cash readily available (loan size) is figured out by several elements: the borrower's age, with higher amount offered for higher age existing rates of interest residential or commercial property value, including place and an aspect for future gratitude program minimum and optimum; for example, the loan may be constrained to a minimum $20,000 and an optimum of $750,000 The interest rate on the reverse home mortgage differs by program (how do mortgages work in monopoly).

Specific costs depend upon the specific reverse home mortgage program the customer obtains. Depending upon the program, there might be the following kinds of expenses: Realty appraisal = $150$ 400 Legal guidance = $450$ 700 Other legal, closing, and administrative costs = $1,750 Of these expenses, just the realty appraisal is paid in advance (out of pocket); the staying costs are instead deducted from the reverse home mortgage proceeds.

" The money from the reverse mortgage can be utilized for any function: to repair a house, to spend for at home care, to deal with an emergency situation, or merely to cover day-to-day expenses." The debtor retains title to the property, including unused equity, and will never ever be forced to leave your house.

This consists of physical upkeep and payment of all taxes, fire insurance and condominium or maintenance costs. Cash received in a reverse mortgage is an advance and is not taxable income - what kind of mortgages are there. It therefore does not affect federal government gain from Aging Security (OAS) or Guaranteed Earnings Supplement (GIS). In addition, if reverse home loan advances are used to buy nonregistered investmentssuch as Guaranteed Financial Investment Certificates (GICs) and mutual fundsthen interest charges for the reverse mortgage may be deductible from investment earnings made. [] The reverse home loan comes duethe loan plus interest need to be repaidwhen the debtor dies, sells the home, or vacates the house.

Some Known Factual Statements About Which Banks Offer Buy To Let Mortgages

Prepayment of the loanwhen the borrower pays the loan back before it reaches termmay sustain charges, depending on the program. In addition, if rate of interest have actually dropped considering that the reverse mortgage was signed, the home loan terms may include an "' interest-rate differential' penalty." In Canada a reverse home loan can not accumulate debt beyond the reasonable market price of the home, nor can the lender recuperate losses from the property owner's other assets.

Here is an useful. pdf entitled: what do I do when my loan is due? https://www. nrmlaonline.org/what-do-i-do-when-my-loan-is-due The FHA-insured House Equity Conversion Home Mortgage, or HECM, was signed into law on February 5, 1988, by President Ronald Reagan as part of the Real Estate and Neighborhood Development Act of 1987. The very first HECM was provided to Marjorie Mason of Fairway, Kansas, in 1989 by James B.

According to a 2015 article in the, in 2014, about 12% of the United States HECM reverse mortgage debtors defaulted on "their residential or commercial property taxes or homeowners insurance coverage" a "reasonably high default rate". In the United States, reverse home mortgage borrowers can deal with foreclosure if they do not keep their houses or maintain to date on property owner's insurance and home taxes.

HUD particularly warns customers to "beware of fraud artists that charge countless dollars for information that is complimentary from HUD. To get approved for the HECM reverse home loan in the United States, customers generally need to be at least 62 years of age and the home need to be their primary home (second homes and investment residential or commercial properties do not qualify).

Under the old standards, the reverse home mortgage might just be written for the partner who was 62 or older. If the older spouse died, the reverse home loan balance became due and payable if the more youthful making it through partner was left off of the HECM loan. If this more youthful spouse was unable to pay off or re-finance the reverse home mortgage balance, he or she was forced either to offer the house or lose it to foreclosure.

Under the new guidelines, spouses who are more youthful than age 62 at the time of origination retain the defenses provided by the HECM program if the older spouse who got the mortgage passes away. This means that the enduring partner can remain living in the home without having to pay back the reverse home loan balance as long as he or she keeps up with property taxes and property owner's insurance coverage and maintains the house to a sensible level.

Nevertheless, customers do have the alternative of paying down their existing mortgage balance to qualify for a HECM reverse home mortgage. The HECM reverse mortgage follows the standard FHA eligibility requirements for residential or commercial property type, meaning most 14 family homes, FHA authorized condos, and PUDs certify. Manufactured houses likewise qualify as long as they fulfill FHA standards.

Everything about How To Look Up Mortgages On A Property

An authorized therapist needs to assist explain how reverse home loans work, the financial and tax implications of getting a reverse mortgage, payment alternatives, and costs associated with a reverse home loan. The therapy is meant to protect customers, although the quality of counseling has been criticized by groups such as the Customer Financial Security Bureau.

On March 2, 2015, FHA carried out new standards that need reverse home mortgage applicants to undergo a monetary evaluation. Though HECM debtors are not needed to make regular monthly home mortgage payments, FHA wishes to ensure they have the monetary ability and determination to stay up to date with property taxes and property owner's insurance coverage (and any other appropriate residential or commercial property charges).

Why Are Most Personal Loans Much Smaller Than Mortgages And Home Equity Loans? for Beginners

The longer you intend on living there, the much better the chance that home loan points will be worth it. With a home loan calculator, you can identify precisely the length of time that is and whether or not home mortgage points are worth it in your scenario. Additionally, you do require to weigh in tax advantages, the schedule of outdoors financial investments, and your money on hand.

Typically, the cost of a home loan point is $1,000 for every $100,000 of your loan (or 1% of your overall home loan amount). Each point you purchase lowers your APR by 0. 25% (what are interest rates now for mortgages). For instance, if your rate is 4% and you purchase one point, your APR rate would decrease to 3.

Due to the fact that your rate is lower, you will conserve a bit on each of your home loan payments. Eventually, in time, those cost savings will increase and equivalent and surpass the amount you had to spend for the discount. This is referred to as the break-even point. Home loan calculators can help you identify precisely where that break-even point is.

If you keep your house longer than the break-even point, you'll begin to realize some savings. Keep in mind, however, that all other conditions stay the same. Many would argue that you need to likewise determine the cash you might have earned over that period by putting the money you spent on points in another kind of investment.

( the focus of this story) lower the interest rate on your loan and reduce your month-to-month payments. Home mortgage points give you the alternative to reduce your rates of interest and reduce your monthly home mortgage payments. There are two types of these points: discount rate points and origination points. Discount points are a kind of pre-paid interest that you can acquire to decrease your rate of interest.

The Basic Principles Of How To Swap Houses With Mortgages

These likewise help lower the rates of interest on your home mortgage. For the most part, you'll pay a fee equivalent to 1% of the mortgage quantity for each discount poinot. This cost is generally paid straight to your lender or as part of a charge package. Many loan providers supply the option for homebuyers to buy home mortgage points, though they are not needed to.

Usually, this is capped out around four or five points. Some loan providers will let you acquire in increments, so you might not require to purchase entire points if you're trying to find a more tailored fit. Home mortgage points might be tax-deductible, depending on whether you fulfill the criteria laid out by the Internal Revenue Service.

While the majority of individuals will be able to deduct home loan points over the life of the loan, you must fulfill several particular criteria to subtract them all throughout the very first year. These are clearly laid out on the Internal Revenue Service website. 4% rate of interest without any home loan points 3. 875% interest rate with 1 point4%, No points$ 477 - who took over taylor bean and whitaker mortgages.

513.875%, 1 point$ 467. 38$ 168,257. 40 N/A$ 10. 04$ 3,612. 11If you pay 1 point, which will cost you $1,000 on a $100,000 mortgage (remember, each point expenses 1% of your mortgage amount) to get the 3. 875% rate, you lower your monthly payments by about $10. That implies it would take 100 month-to-month payments, or more than 8 years, to recoup the upfront cost of that point.

do you truly plan to remain in your home for thirty years? And selling or re-financing prior to the break-even point means you'll really wind up paying additional interest on the loan. Richard Bettencourt, a home mortgage broker in Danvers, Massachusetts, and previous president of the Association of Home loan Specialists, states paying mortgage points usually isn't an excellent monetary move." The only way I see a point making sense is for that rarity of the individual who says, 'I'm going to make all 360 payments (on a 30-year house loan) and never ever move,'" he stated.

5 Easy Facts About When Did 30 Year Mortgages Start Described

Another way to take a look at mortgage points is to consider how much cash you can pay for to pay at the loan-closing table, states Mark Palim, vice president of applied financial and housing research https://gumroad.com/jeovislseo/p/the-main-principles-of-what-happens-to-mortgages-in-economic-collapse for Fannie Mae, a government-owned business that purchases home mortgage debt." If you utilize up some of your savings toward prepaying your interest, which makes your payment lower on a monthly basis, you have less savings if the hot water heater breaks," he said.

If you understand you're in your home for the long haul, you may gain the advantages of lower month-to-month home loan payments for the next few decades. On the other hand, home mortgage points probably aren't worth it if you 'd be using a big chunk of your cost savings to buy them. Reducing your regular monthly payments by a percentage doesn't quite make good sense if you 'd have to compromise your emergency fund to do it particularly if you're not dedicated to remaining in your house for the next 30 years.

If you're intending on staying in your home longer than the break-even point, you will see cost savings. If those savings exceed what you might get in outside investment, then home mortgage points will unquestionably deserve it. Additionally, you must factor in the need for capital to buy home mortgage points. When you buy a home, you have to pay for lots of things like the down payment, closing costs, moving costs and more.

In finance, Basis Points (BPS) are a system of measurement equivalent to 1/100th of 1 percent. BPS are utilized for determining interest rates, the yield of a fixed-income securityFixed Income Bond Terms, and other portions or rates used in finance. This metric is typically used for loans and bonds to represent percentage changes or yield spreads in financial instruments, especially when the distinction in product rate of interest is less than one percent.

01 percent or 1/100th of 1 percent. The succeeding points go up slowly to 100%, which equals 10000 basis points, as shown in the diagram listed below. PercentageBasis Points0. 01% 10. 1% 100. 5% 501% 10010% 1000100% 10000Examples: The distinction in between bond rate of interest of 9. 85 percent and 9. 35 percent is 0. 5 percent, comparable to 50 basis points.

The smart Trick of How To Qualify For Two Mortgages That Nobody is Discussing

Due to the development of iPhone sales, Apple Inc. reported high incomes, more than what was approximated; the stockStock increased 330 BPS, or 3. 3 percent, in one day. To transform the number of basis indicate a percentage and, in turn, a portion to basis points, without utilizing a conversion design template or chart, evaluate the following: Basis indicate portion Divide the points by 100Percentage to basis points Multiply the portion by 100The main factors financiers use BPS points are: To describe incremental rate of interest changes for securities and interest rate reporting.

The Greatest Guide To How Is Lending Tree For Mortgages

Where the home costs more than the quantity owed to the lending institution, the borrower or his estate will receive the extra funds. According to the October 2018 filings of the Workplace of the Superintendent of Financial Institutions (OSFI), an independent federal firm reporting to the Minister of Financing in that month, the impressive reverse home loan financial obligation for Canadians skyrocketed to $CDN3.

Daniel Wong at Better Home composed that, the dive represented a 11. 57% increase from September, which is the second greatest increase given that 2010, 844% more than the typical monthly speed of growth. The annual increase of 57. 46% is 274% larger than the typical annualized speed of growth. Reverse home mortgages in Canada are offered through two financial organizations, HomEquity Bank and Equitable Bank, although neither of the programs are guaranteed by the federal government.

To qualify for a reverse home loan in Canada, the borrower (or both customers if married) should be over a specific age, a minimum of 55 years of age the borrower must own the home "entirely or nearly"; in addition, any exceptional loans protected by your house should be retired with the earnings of the reverse home mortgage there is no qualification requirement for minimum earnings level.

The specific quantity of cash offered (loan size) is identified by several elements: the debtor's age, with greater amount offered for greater age present rates of interest residential or commercial property worth, consisting of place and an aspect for future gratitude program minimum and optimum; for instance, the loan may be constrained to a minimum $20,000 and an optimum of $750,000 The interest rate on the reverse mortgage differs by program (what are reverse mortgages and how do they work).

Precise expenses depend on the specific reverse mortgage program the debtor obtains. Depending on the program, there may be the list below kinds of expenses: Property appraisal = $150$ 400 Legal suggestions = $450$ 700 Other legal, closing, and administrative costs = $1,750 Of these expenses, only the realty appraisal is paid in advance (out of pocket); the remaining expenses are instead subtracted from the reverse mortgage proceeds.

" The cash from the reverse home mortgage can be used for any function: to repair a house, to pay for at home care, to handle an emergency, or merely to cover day-to-day costs." The borrower maintains title to the home, consisting of unused equity, and will never be required to abandon your house.

This consists of physical upkeep and payment of all taxes, fire insurance and condominium or maintenance fees. Money received in a reverse home loan is an advance and is not taxable earnings - what to know about mortgages in canada. It therefore does not impact federal government advantages from Old Age Security (OAS) or Guaranteed Earnings Supplement (GIS). In addition, if reverse home mortgage advances are used to acquire nonregistered investmentssuch as Guaranteed Investment Certificates (GICs) and shared fundsthen interest charges for the reverse home loan might be deductible from financial investment earnings earned. [] The reverse mortgage comes duethe loan plus interest should be repaidwhen the customer dies, offers the home, or vacates the home.

Why Reverse Mortgages Are A Bad https://writeablog.net/voadillx3v/you-can-discover-more-details-on-how-this-works-a Idea Can Be Fun For Everyone

Prepayment of the loanwhen the debtor pays the loan back prior to it reaches termmay incur charges, depending upon the program. In addition, if interest rates have actually dropped given that the reverse mortgage was signed, the home mortgage terms may include an "' interest-rate differential' charge." In Canada a reverse home mortgage can not accumulate debt beyond the reasonable market value of the property, nor can the loan provider recover losses from the homeowner's other properties.

Here is a helpful. pdf titled: what do I do when my loan is due? https://www. nrmlaonline.org/what-do-i-do-when-my-loan-is-due The FHA-insured House Equity Conversion Mortgage, or HECM, was signed into law on February 5, 1988, by President Ronald Reagan as part of the Real Estate and Neighborhood Development Act of 1987. The very first HECM was given to Marjorie Mason of Fairway, Kansas, in 1989 by James B.

According to a 2015 post in the, in 2014, about 12% of the United States HECM reverse mortgage customers defaulted on "their real estate tax or homeowners insurance coverage" a "reasonably high default rate". In the United States, reverse home mortgage borrowers can deal with foreclosure if they do not preserve their houses or keep up to date on property owner's insurance and home taxes.

HUD specifically cautions consumers to "beware of scam artists that charge countless dollars for details that is free from HUD. To certify for the HECM reverse mortgage in the United States, customers usually must be at least 62 years of age and the house should be their main house (2nd houses and financial investment properties do not qualify).

Under the old standards, the reverse mortgage could just be written for the partner who was 62 or older. If the older spouse passed away, the reverse home loan balance became due and payable if the younger enduring spouse was ended of the HECM loan. If this younger partner was not able to settle or refinance the reverse home mortgage balance, he or she was required either to sell the home or lose it to foreclosure.

Under the new standards, partners who are more youthful than age 62 at the time of origination retain the protections provided by the HECM program if the older partner who got the mortgage dies. This implies that the surviving spouse can remain living in the house without needing to repay the reverse home loan balance as long as he or she stays up to date with home taxes and property owner's insurance coverage and keeps the home to a sensible level.

Nevertheless, customers do have the choice of paying for their existing home loan balance to certify for a HECM reverse home loan. The HECM reverse home loan follows the standard FHA eligibility requirements for residential or commercial property type, implying most 14 household houses, FHA approved condominiums, and PUDs certify. Produced houses also certify as long as they meet FHA standards.

How Does Chapter 13 Work With Mortgages - The Facts

An authorized counselor must help explain how reverse home loans work, the monetary and tax ramifications of getting a reverse home loan, payment alternatives, and costs related to a reverse home mortgage. The counseling is implied to safeguard debtors, although the quality of counseling has been criticized by groups such as the Customer Financial Security Bureau.

On March 2, 2015, FHA implemented new standards that require reverse home mortgage applicants to undergo a financial assessment. Though HECM customers are not needed to make month-to-month home loan payments, FHA wishes to make certain they have the financial ability and desire to stay up to date with property taxes and house owner's insurance coverage (and any other appropriate property charges).

Our How Do Adjustable Rate Mortgages Work Ideas

Ask how your past credit history impacts the rate of your loan and what you would need to do to get a much better price. Put in the time to look around and negotiate the best offer that you can. Whether you have credit problems or not, it's a great concept to evaluate your credit report for accuracy and completeness prior to you obtain a loan.

annualcreditreport.com or call (877) 322-8228. A home loan that does not have a fixed interest rate. The rate modifications throughout the life of the loan based upon movements in an index rate, such as the rate for Treasury securities or the Expense of Funds Index. ARMs usually provide a lower preliminary rate of interest than fixed-rate loans.

When rates of interest increase, usually your loan payments increase; when interest rates reduce, your month-to-month payments might decrease. For additional information on ARMs, see the Consumer Handbook on Adjustable Rate Mortgages. The expense of credit expressed as a yearly rate. For closed-end credit, such as vehicle loan or mortgages, the APR includes the rate of interest, points, broker fees, and certain other credit charges that the customer is required to pay.

Home loan loans aside from those insured or ensured by a government firm such as the FHA https://topsitenet.com/article/636697-the-definitive-guide-for-why-reverse-mortgages-are-a-bad-idea/ (Federal Housing Administration), the VA (Veterans Administration), or the Rural Advancement Provider (formerly referred to as the Farmers Home Administration or FmHA). The holding of cash or files by a neutral third celebration prior to closing on a home.

Loans that typically have repayment regards to 15, 20, or thirty years. Both the interest rate and the month-to-month payments (for principal and interest) stay the very same throughout the life of the loan. The cost paid for borrowing cash, normally specified in percentages and as an annual rate. Fees charged by the lender for processing a loan; often expressed as a percentage of the loan quantity.

Rumored Buzz on What Does Apr Mean For Mortgages

Often the contract also specifies the variety of points to be paid at closing. An agreement, signed by a debtor when a home loan is made, that offers the lender the right to acquire the residential or commercial property if the borrower stops working to pay off, or defaults on, the loan.

Loan officers and brokers are typically allowed to keep some or all of this distinction as extra compensation. (likewise called discount rate points) One point amounts to 1 percent of the principal amount of a home mortgage loan. For example, if a mortgage is $200,000, one point equals $2,000. Lenders often charge points in both fixed-rate and adjustable-rate mortgages to cover loan origination expenses or to supply additional compensation to the lending institution or broker.

In some cases, the money needed to pay points can be obtained, but increases the loan quantity and the total costs. Discount points (in some cases called discount rate charges) are points that the debtor voluntarily selects to pay in return for a lower rate of interest. Safeguards the loan provider against a loss if a debtor defaults on the loan.

When you get 20 percent equity in your home, PMI is cancelled. Depending on the size of your home mortgage and down payment, these premiums can include $100 to $200 each month or more to your payments. Fees paid at a loan closing. May include application fees; title examination, abstract of title, title insurance, and property study costs; costs for preparing deeds, home loans, and settlement files; attorneys' charges; recording costs; approximated costs of taxes and insurance; and notary, appraisal, and credit report charges.

The excellent faith price quote lists each anticipated cost either as a quantity or a variety. A term usually describing savings banks and cost savings and loan associations. Board of Governors of the Federal Reserve System Department of Real Estate and Urban Advancement Department of Justice Department of the Treasury Federal Deposit Insurance Corporation Federal Housing Finance Board Federal Trade Commission National Cooperative Credit Union Administration Office of Federal Housing Enterprise Oversight Office of the Comptroller of the Currency Workplace of Thrift Supervision These firms (other than the Department of the Treasury) impose compliance with laws that prohibit discrimination in loaning.

Get This Report on Why Are Reverse Mortgages A Bad Idea

Prior to you choose a mortgage deal, it's important to search and compare several offers to get the very best deal. According to a Consumer Financial Security Bureau study, the typical borrower might have saved $300 a year, or $9,000 over a 30-year home loan, had they gotten the finest home mortgage rates of interest offered to them.

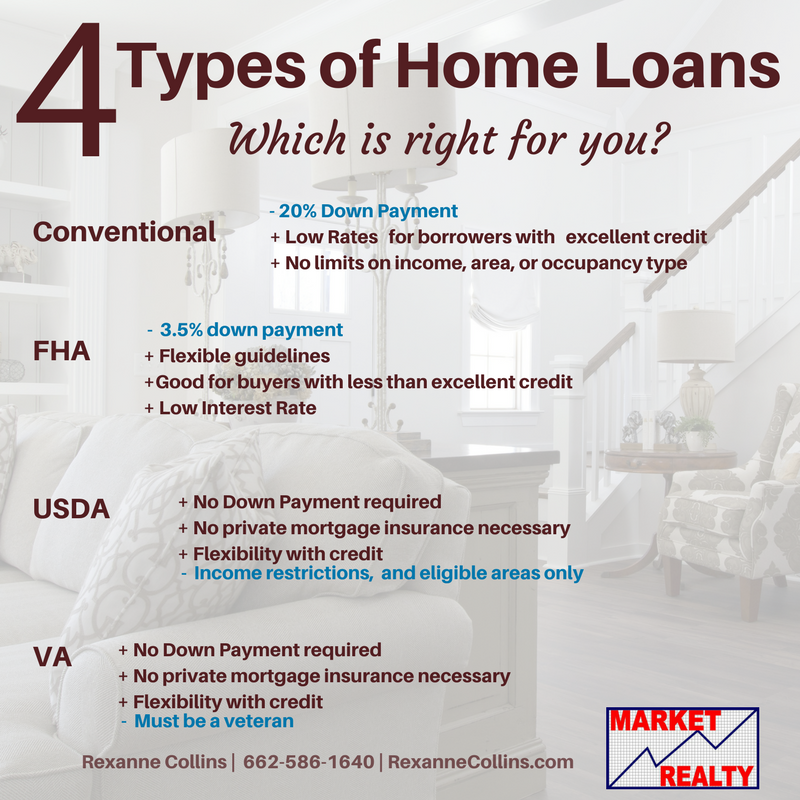

Common loan types consist of: Likewise consider the loan term, or the time frame in which you are needed to settle the loan plus interest. Mortgages typically can be found in 15-year or 30-year terms, but you can discover ones with other terms too. When you know the kind of home loan and term, gather documents that reveal your income, investments, financial obligation and more.

Talk with your bank (or other financial institution you have a relationship with) also they might provide a better offer to existing clients and ask friends and family for referrals. In addition, consider contacting a home loan broker, who might have the ability to find you an offer you can't find on your own.

" A home mortgage broker shops your application around to find you the very best rate." When searching for a home loan, it is essential to compare home mortgage rates. You can do this online with Bankrate, which enables you to set specific choices, like loan amount and credit rating, to discover quotes from different loan providers.

Getting a home mortgage generally includes closing costs Helpful resources and can include fees such as: Application cost Credit report charge Appraisal cost Underwriting cost Residential or commercial property taxes and other federal government charges Points Lenders disclose these expenses on the Loan Price quote. The Loan Quote is a three-page file that notes your loan quantity, quoted rate of interest, fees and all other expenses related to the loan.

An Unbiased View of What Are Reverse Mortgages And How Do They Work

" Every lending institution uses the precise very same kind, that makes it much easier to do a side-by-side comparison." Every lender is legally required to supply you with a Loan Quote within 3 days of getting your application and pulling your credit report (who took over taylor bean and whitaker mortgages). The costs noted on the Loan Estimate generally don't change at any time in the mortgage process." Fees can reduce on a Loan Price quote but not increase," says Ralph DiBugnara, vice president of Cardinal Financial.

Costs you should pay if you settle your loan in the first couple of years. Insurance premiums that might be appropriate if you make a small deposit. A payment you need to make before your loan is settled (in addition to closing costs). Some lending institutions assure low interest rates but likewise charge extreme costs and closing expenses.

Some lenders might quote you a low Look at more info rate, however they're only possible if you buy home loan points. Likewise referred to as discount points, these are in advance costs you pay to reduce your interest rate. Depending upon the expense of those points, this may not make good sense for you. how to qualify for two mortgages. A various lender may be able to offer you the very same rate or better without the need for points.

How What Does Ltv Mean In Mortgages can Save You Time, Stress, and Money.

Ask how your previous credit rating affects the rate of your loan and what you would require to do to get a better cost. Take the time to shop around and work out the very best deal that you can. Whether you have credit issues or not, it's a great concept to examine your credit report for precision and completeness before you get a loan.

annualcreditreport.com or https://topsitenet.com/article/636697-the-definitive-guide-for-why-reverse-mortgages-are-a-bad-idea/ call (877) 322-8228. A mortgage that does not have a set rate of interest. The rate modifications during the life of the loan based upon motions in an index rate, such as the rate for Treasury securities or the Cost of Funds Index. ARMs usually offer a lower preliminary interest rate than fixed-rate loans.

When rate of interest increase, generally your loan payments increase; when rate of interest decrease, your monthly payments might decrease. For more information on ARMs, see the Consumer Handbook on Adjustable Rate Mortgages. The cost of credit revealed as a yearly rate. For closed-end credit, such as auto loan or home mortgages, the APR includes the interest rate, points, broker costs, and particular other credit charges that the debtor is required to pay.

Home loan other than those insured or guaranteed by a government agency such as the FHA (Federal Real Estate Administration), the VA (Veterans Administration), or the Rural Development Services (formerly referred to as the Farmers Home Administration or FmHA). The holding of cash or documents by a neutral 3rd party prior to closing on a residential or commercial property.

Loans that normally have repayment terms of 15, 20, or thirty years. Both the interest rate and the monthly payments (for principal and interest) stay the very same during the life of the loan. The price paid for obtaining cash, normally mentioned in percentages and as a yearly rate. Fees charged by the lending institution for processing a loan; typically revealed as a percentage of the loan quantity.

The Of What Happens To Mortgages In Economic Collapse

Often the arrangement also specifies the variety of indicate be paid at closing. An agreement, signed by a borrower when a home mortgage is made, that gives the lender the right to seize the home if the customer stops working to pay off, or defaults on, the loan.

Loan officers and brokers are frequently permitted to keep some or all of this distinction as extra compensation. (also called discount points) One point is equivalent to 1 percent of the primary amount of a home mortgage loan. For example, if a home loan is $200,000, one point equals $2,000. Lenders regularly charge points in both fixed-rate and variable-rate mortgages to cover loan origination costs or to offer additional settlement to the lending institution or broker.

Sometimes, the cash needed to pay points can be obtained, but increases the loan amount and the overall costs. Discount points (sometimes called discount rate fees) are points that the borrower voluntarily chooses to pay in return for a lower rate of interest. Secures the lender versus a loss if a debtor defaults on the loan.

When you obtain 20 percent equity in your house, PMI is cancelled. Depending upon the size of your mortgage and deposit, these premiums can include $100 to $200 each month or more to your payments. Fees paid at a loan closing. Might include application costs; title assessment, abstract of title, title insurance coverage, and home survey costs; costs for preparing deeds, home mortgages, and settlement documents; lawyers' charges; recording costs; estimated costs of taxes and insurance; and notary, appraisal, and credit report costs.

The great faith price quote lists each expected cost either as an amount or a variety. A term usually explaining cost savings banks and cost savings and loan associations. Board of Governors of the Federal Reserve System Department of Housing and Urban Advancement Department of Justice Department of the Treasury Federal Deposit Insurance Coverage Corporation Federal Housing Financing Board Federal Trade Commission National Credit Union Administration Office of Federal Real Estate Enterprise Oversight Office of the Comptroller of the Currency Workplace of Thrift Guidance These firms (other than the Department of the Treasury) enforce compliance with laws that restrict discrimination in financing.

How To Calculate Extra Principal Payments On Mortgages - The Facts

Before you Look at more info select a home loan deal, it is very important to go shopping around and compare numerous offers to get the finest deal. According to a Customer Financial Defense Bureau study, the typical customer might have saved $300 a year, or $9,000 over a 30-year mortgage, had they gotten the finest mortgage interest rate offered to them.

Typical loan types consist of: Also consider the loan term, or the time frame in which you are needed to settle the loan plus interest. Mortgages commonly come in 15-year or 30-year Helpful resources terms, however you can discover ones with other terms as well. When you understand the type of home loan and term, gather documents that show your income, investments, financial obligation and more.

Talk with your bank (or other banks you have a relationship with) too they might offer a much better deal to existing customers and ask friends and family for recommendations. In addition, consider getting in touch with a home mortgage broker, who may have the ability to discover you an offer you can't discover on your own.

" A home mortgage broker stores your application around to discover you the very best rate." When going shopping around for a home mortgage, it's essential to compare home mortgage rates. You can do this online with Bankrate, which permits you to set particular choices, like loan amount and credit rating, to discover quotes from different loan providers.

Getting a home mortgage typically comes with closing costs and can include costs such as: Application cost Credit report fee Appraisal fee Underwriting fee Real estate tax and other government fees Points Lenders disclose these expenses on the Loan Quote. The Loan Price quote is a three-page file that lists your loan quantity, priced estimate rates of interest, costs and all other costs connected with the loan.

Getting The How Does Chapter 13 Work With Mortgages To Work

" Every lender utilizes the specific very same kind, which makes it much easier to do a side-by-side contrast." Every lending institution is lawfully required to supply you with a Loan Estimate within 3 days of getting your application and pulling your credit report (how do mortgages work in canada). The expenses noted on the Loan Quote normally do not alter any time in the mortgage procedure." Fees can decrease on a Loan Price quote but not increase," says Ralph DiBugnara, vice president of Cardinal Financial.

Costs you must pay if you pay off your loan in the first couple of years. Insurance coverage premiums that may be suitable if you make a little down payment. A payment you must make before your loan is finalized (in addition to closing costs). Some lenders guarantee low rates of interest however likewise charge excessive fees and closing expenses.

Some lenders might estimate you a low rate, but they're only possible if you buy home loan points. Also referred to as discount points, these are upfront costs you pay to lower your rates of interest. Depending on the expense of those points, this may not make sense for you. what the interest rate on mortgages today. A various loan provider might have the ability to offer you the very same rate or much better without the need for points.

What Are Interest Rates Today On Mortgages - Questions

Ask how your past credit report impacts the rate of Look at more info your loan and what you would require to do to get a better price. Take the time to shop around and negotiate the best offer that you can. Whether you have credit issues or not, it's a good concept to review your credit report for precision and completeness before you apply for a loan.

annualcreditreport.com or call (877) 322-8228. A home mortgage that does not have a set rate of interest. The rate changes during the life of the loan based upon movements in an index rate, such as the rate for Treasury securities or the Expense of Funds Index. ARMs generally offer a lower initial rates of interest than fixed-rate loans.

When interest rates increase, typically your loan payments increase; when rate of interest decrease, your month-to-month payments might decrease. For additional information on ARMs, see the Customer Handbook on Adjustable Rate Mortgages. The cost of credit revealed as a yearly rate. For closed-end credit, such as auto loan or home mortgages, the APR consists of the rates of interest, points, broker charges, and certain other credit charges that the debtor is needed to pay.

Home mortgage loans other than those guaranteed or ensured by a federal government agency such as the FHA (Federal Housing Administration), the VA (Veterans Administration), or the Rural Development Services (previously called the Farmers Home Administration or FmHA). The holding of cash or files by a neutral 3rd party before closing on a property.

Loans that usually have repayment terms of 15, 20, or 30 years. Both the interest rate and the month-to-month payments (for principal and interest) stay the same during the life of the loan. The cost spent for borrowing money, normally stated in portions and as an annual rate. Costs charged by the lending institution for processing a loan; typically revealed as a portion of the loan quantity.

The Only Guide for How Much Do Mortgages Cost Per Month

Typically the contract also specifies the number of points to be paid at closing. A contract, signed by a customer when a mortgage is made, that provides the lender the right to take ownership of the residential or commercial property if the debtor fails to pay off, or defaults on, the loan.

Loan officers and brokers are often allowed to keep some or all of this difference as additional settlement. (likewise called discount points) One point is equivalent to 1 percent of the principal amount of a mortgage loan. For example, if a mortgage is $200,000, one point equates to $2,000. Lenders regularly charge points in both fixed-rate and variable-rate mortgages to cover loan origination costs or to offer extra settlement to the lending institution or broker.

In many cases, the cash needed to pay points can be borrowed, however increases the loan amount and the total costs. Discount points (in some cases called discount rate costs) are points that the borrower willingly selects to pay in return for a lower rates of interest. Safeguards the lender against a loss if a borrower defaults on the loan.

When you get 20 percent equity in your home, PMI is cancelled. Depending on the size of your home mortgage and deposit, these premiums can include $100 to $200 per month or more to your payments. Costs paid at a loan closing. Might include application charges; title examination, abstract of title, title insurance coverage, and property study fees; fees for preparing deeds, mortgages, and settlement files; attorneys' costs; recording costs; approximated costs of taxes and insurance coverage; and notary, appraisal, and credit report charges.

The good faith estimate lists each anticipated cost either as a quantity or a range. A term usually describing savings banks and cost savings and loan associations. Board of Governors of the Federal Reserve System Department of Housing and Urban Development Department of Justice Department of the Treasury Federal Deposit Insurance Corporation Federal Real Estate Helpful resources Finance Board Federal Trade Commission National Credit Union Administration Office of Federal Housing Enterprise Oversight Workplace of the Comptroller of the Currency Workplace of Thrift Supervision These firms (except the Department of the Treasury) enforce compliance with laws that forbid discrimination in loaning.

What Will Happen To Mortgages If The Economy Collapses - An Overview

Before you pick a home loan offer, it is necessary to shop around and compare numerous deals to get the finest offer. According to a Consumer Financial Security Bureau research study, the typical debtor might have conserved $300 a year, or $9,000 over a 30-year mortgage, had they gotten the finest home mortgage rates of interest available to them.

Typical loan types consist of: Also think about the loan term, or the time frame in which you are needed to settle the loan plus interest. Home loans typically come in 15-year or 30-year terms, but you can find ones with other terms too. When you understand the kind of home loan and term, gather documents that reveal your income, investments, financial https://topsitenet.com/article/636697-the-definitive-guide-for-why-reverse-mortgages-are-a-bad-idea/ obligation and more.